“In the dust choked markets on the outskirts of Kenya’s capital, the most valuable tool Wangari owns is not her plough or her scales. It is a battered smartphone with a cracked screen.

For years, Wangari lived at the mercy of the cash lag. She waited days for buyers to arrive with physical notes. She lived in fear of the thieves who stalked the payday trails. She watched her children go hungry while her earnings sat locked in the pockets of distant middlemen. To the ivory towered banks in the city centre, Wangari was invisible, a high-risk ghost without a paper trail.”

Some Mobile Network Operators (MNO) asked themselves the question - What if the network served the people, rather than the people serving financial intermediaries or banks?

OVER 10 YEARS telcos such as Vodacom, MTN, Safaricom and Orange developed and deployed MOBILE MONEY for customers, those without access to bank accounts ,and today have defined how Africa builds financial systems not just for high income customers but low and lower-middle income customers like Wangari who can benefit from: -

• Instant settlement: Payments land in seconds, not days.

• Zero paperwork: A credit score is written with every transaction

For Wangari, this is not about fintech or disruption. It is about the fact that the device already in her hand has finally given her the one thing the world’s banks never could: freedom.”

Quoted from Jean Pierre Mugenga ‘When Poverty Meets Innovation: Five Technologies Rewriting the Rules of Survival’

Let’s examine future potential:-

- Digital wallets, Global reach: Finance without banks

- Incumbent gorillas in the market have a head start

- New partnership opportunities

- Who will win the race?

- Concluding thoughts

1.Digital Wallets, Global Reach: Finance Without Banks

Today the African market is in a new phase of extending inclusive access to digital payments and financial services lead by a variety of players:

- Telco led digital wallets from Mobile Network Operators (MNOs) and Mobile Virtual Mobile Operators (MVNOs) accessed from subscribers smartphones

- Bank led digital wallets from commercial banks, currently focussed on urban customers

- Aggregators and API enablers- connecting and integrating telcos, banks, payment platforms and Fintechs/insurtech’s

- Payment orchestration platforms unifying mobile money, banks, payment rails, credit cards onto one technology stack

- Fintech led initiatives- loans, savings, micro-services & contracting

The Next Phase- Adding more financial services to existing mobile money capabilities

- Embedded Finance – Loans, Savings, , Pensions, Life, Insurance

- Interoperable Digital wallets- across Borders and Networks

- AI enhanced fraud protection – transaction monitoring, proof of intent

- Designing payment architecture around mobile money interoperability, scalability and compliance

- DEFINING how Africa builds Financial Systems free from the expensive Western Economies business models

2. Incumbent Gorillas in the market have a head start

Africa is a continent of many countries all with different cultures, regulatory frameworks, sizes of economies and technological maturity. Mobile money deployment is concentrated in a small number of countries with Kenya in a leading position with a half of all financial transactions being processed via M-PESA

- East Africa: Kenya, Tanzania, Uganda

- West Africa: Ghana, Nigeria, Cote d’Ivoire

- Central & South Africa: RSA

- North Africa: Egypt

Safaricom launched M-PESA in 2007; MNO with MoMo has similarly deployed mobile money as has Orange with Orange Pay. Vodacom has a large stake in Safaricom and its own service Vodapay

Success requires critical mass; -

- Strong network of merchants- agents

- Large customer base of mobile subscribers

- PIN based authentication

- Confirmation loop of payments made and received for transparency

- Telco MNO with MoMo has similarly deployed mobile money as has Orange with Orange Pay. Vodacom has a large stake in Safaricom and its own service Vodapay

3. New Partnership Opportunities

MNOs and MVNOs

The strength of incumbent MNOs lies in substantial infrastructure, and each is deploying in more countries. But they are then competing against local telcos who know the market and Fintechs keen to offer financial services. Innovation is speeding up and MVNOs have an advantage in that they are unencumbered by having to run enterprise architecture infrastructure as they license spare capacity from MNOs.

There is a $150BN revenue (see Further Reading) opportunity for the MNOs and/or MVNOs that can accelerate the acquisition of new customers. The winning partnerships will be those that orchestrate:

- Telco platforms

- Payment gateways

- Compliance systems

- Settlement layers

- Card networks

- API connected ecosystems of lenders, saving accounts, insurance, micro-contracting

Mobile Money has outpaced traditional banking and Online Payment apps outside the densely populated urban areas. With its inclusive approach it has bought millions into a formal financial ecosystem and in parallel sheltered customers from backend complexity via user friendly smartphone UX.

Over the next 5 years Mobile Money can onboard millions more customers and be the frontend access to the wide range of payment and financial services. An everyday financial tool from the subscribers’ phones at affordable prices that even low-income customers can adopt including those on $15-$25 a day giving them the opportunity to live and trade and so grow their incomes and ,in aggregate, country GDP.

Commercial Banks

Banks have enjoyed the high prices richer city dwellers can afford and will have a nasty awakening as the wide range of financial services at lower pricing will attract middle and high-income customers. Telcos have already leapfrogged banks for low-income and lower-middle-income customers.

Banks already offer digital wallets but these online pay apps are best suited to the urban customer with access to online and branch banking. Internet connectivity is vital but in many rural areas unreliable or not accessible. Commercial banks could partner with telcos to reach areas out of their reach but then face the threat of the telcos’ mobile money services being more attractive.

Some commentators see the convergence of mobile money wallets and online pay apps with mobile money being the entry point for customers. The strength of any telco-bank partnerships lies in aligned goals. Would a bank give up its protective moat around the urban customer base they have? They might have to as telcos target urban areas without the need for a branch network and its associated costs.

One route would be for banks to acquire or establish wholly owned MVNOs as Revolute, Monzo and N26 have announced. But will traditional banks across Africa have the culture, talent, resources and ambition to be successful?

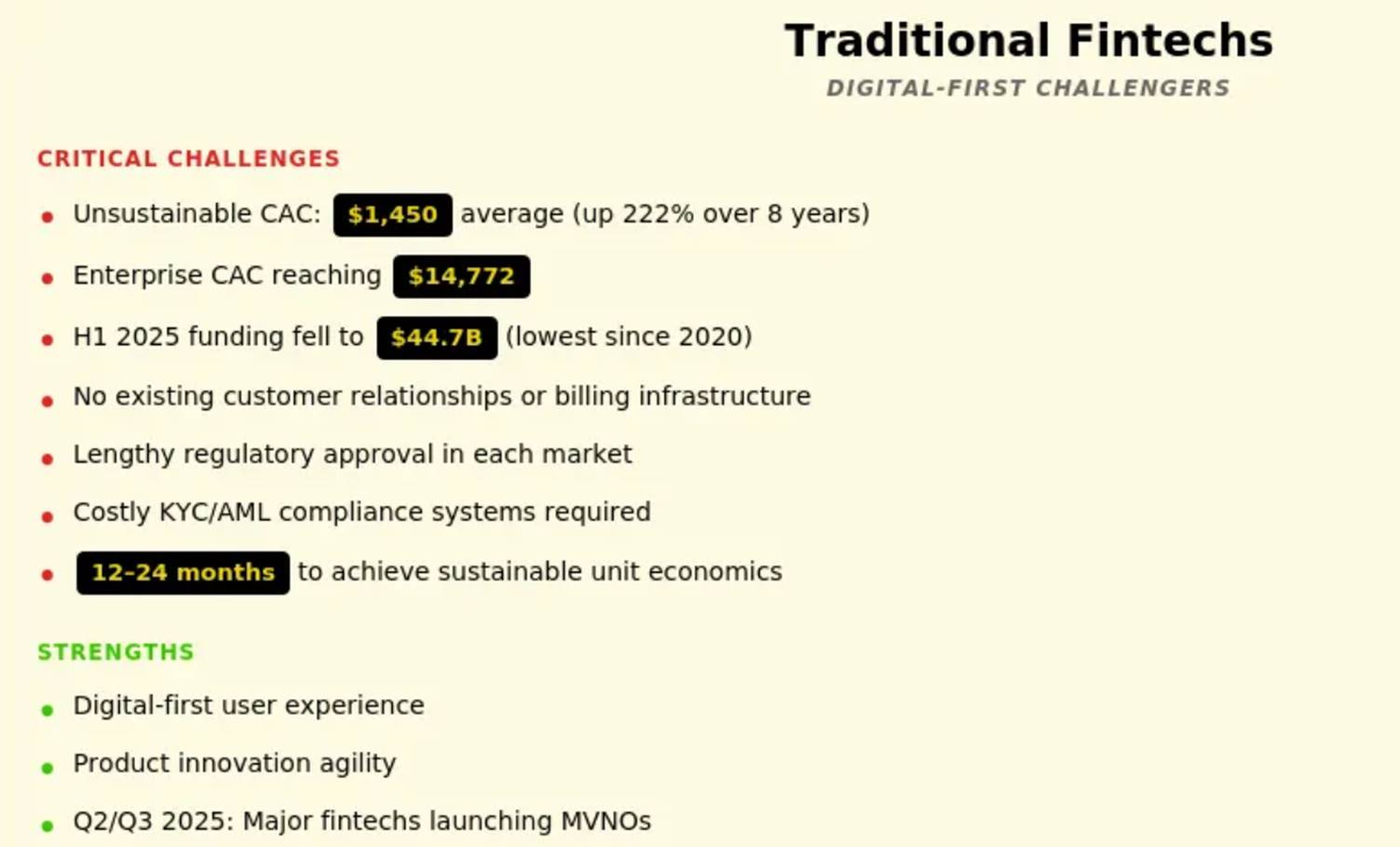

Fintechs

Whilst Fintechs have the strengths of digital first UX, and product innovation agility there are many hurdles to overcome as Mike McLaren illustrates.

Again, launching or converging with MNOs and/or MVNOs is a credible strategy

“The convergence isn’t just about traditional financial services anymore. MVNOs are becoming the natural distribution layer for Web3 financial products, where the SIM card becomes the wallet and the network becomes the bank,” notes Chris Surdak, CEO of ReLeaf Financial.

The tech giants of the US and Europe are an over-costly solution for this market so look out for the local partners used to innovating with scarce resources but delivering high-value services.

4. Who will win the race?

There are two scenarios to consider:

- Current countries where mobile money is widely deployed

- Remaining countries with low or no mobile money penetration

Current countries with widely-deployed mobile money

The key to success lies in mobile money being the front-end entry point for consumers, sole traders and SMEs. MNOs have the incumbents advantage but if they sit on their laurels, they may see the innovation train leave without them and a cold platform is not a comfortable place to stay on. McLaren posits that there is an eighteen-to-twenty-four-month window for these MNOs to orchestrate and deliver the wide range of future financial services customers will demand and described earlier. Not just consumers but small traders and SMEs.

MVNOs will eye these markets greedily should MNOs be slow off the mark.

Countries with low mobile money penetration

Mike McLaren makes a strong case for MVNOs having the speed to market and capabilities to orchestrate the financial services ecosystem. Many are already partnering with strong brand names in retail in which the retailer can sell phones and tablets and, via the MVNO ,a range of financial services. If consumers trust these NVNO and Affinity Partner combinations, they could win the race.

Wesley Hellyar on LinkedIn today said “At MWC in Barcelona, the GSMA Handset Affordability Coalition just moved the needle by earmarking six African nations for a $40 device pilot. As someone deeply embedded in the African telecoms and MVNO space, I see this as a necessary (but incomplete) victory.”

Tailored mobile service plans are key to success and MVNOs with affinity partnerships with brands and enterprises are in a good position to deliver that. MPESA and MoMo have a proven business model for lower-income subscribers so a combination of thyese smartphone subscriptions and $40 devices is a sound foundation.

Why not the MNO? They have the current market for mobile money and the expertise, but they also must contend with adapting core technologies and stacks where APIs are often customised and integration complicated. That could delay the next innovation phase.

They could look to aggregators to help them or, as a vital supplier of mobile voice & data subscriptions, to MVNOs to combine forces for the best of both worlds.

The winners will be the converging partnerships that deliver optimal business models that offer compelling payment and financial services from the smartphone. Whilst I have described the Sub-Saharan Africa market, the potential is also there in Latin America and Asia.

Douglas Laney wrote an article for Forbes describing the global unbanked market of 2 BN new customers! (see related articles below).

Many of the telcos are majority owned by traditional European and American enterprises e.g. Orange and Vodafone. That offers a reverse infiltration of so-called developed countries with these innovative and lower-cost solutions. The UK’s BT, a sleepy giant with its own MNO and MVNO, has set out ambitious goals to leapfrog incumbent European telcos and could exploit these options. That would make for an interesting case study.

Conclusion

No one type of player will win the race, rather an emerging ecosystem of partnerships with MNO collaboration a powerful combination.

Various technologies now enhance such collaboration

- Internet without wires – Starlink connecting rural communities

- Light in the darkness-power without grids-Sun King solar panels

- Wings Over Impassable Roads: Deliveries That Save Lives- Zipline

- Digital Wallets with Proof of Intent – ReLeaf Financial- for trusted transactions

- Eyes in the Machine: Diagnosis Without Doctors- AI diagnostics

One thing is for certain is that telcos have leapfrogged banks in rural areas and can also target the urban customer. Which other partners will coalesce around these foundational platforms?

Related articles

The $150BN blind spot- Why MVNOs Will Win the Next Fintech Revolution Mike McLaren in Medium

When Poverty Meets Innovation: Five Technologies Rewriting the Rules of Survival by Jean Pierre Mugenga

Telcos are becoming banks for the next 2 billion customers by Douglas Laney in Forbes Mag

Remember the future: The next frontier for African telcos McKinsey

MNO & MVNO Partnerships: From Old Fears to New Revenue Allan Rasmussen

“Why Mobile Money Is the Fastest Adoption Channel in Emerging Markets?” For African fintech CEOs and CTOs, this is not a theoretical question. It shows up in your transaction data. If you are focusing on fintech inclusion in an emerging market, chances are your customers are already using mobile money, whether you design for it or not.

https://www.digipay.guru/blog/mobile-money-adoption-strategies-startups-emerging-markets/

unknownx500

unknownx500